HIGH YIELD SAVINGS, CDS, MONEY MARKETS AND MORE: 7 CONSERVATIVE INVESTMENTS THAT YIELD UP TO 3.7%. 1H 2023 EDITION.

Summary: Short Term Treasuries are still the most attractive after tax, nominally protected option for almost all investors.

It can be helpful to think of investing as a ladder of options. At the very bottom of the ladder, the most conservative options are what we call cash-like instruments. This includes including actual dollar bills, high yield savings accounts, no penalty CDs, money market funds, other liquid accounts, cash-like funds, and short-term federal and municipal bonds. At the time of this writing, these all return between 3% and 5% before tax and inflation. We’ve seen a dramatic increase in the returns on these funds in the last few years.

I continue to be shocked by how often you need to manage and move your short term/liquid cash to “optimize” for taxes and yields. To give you a sense of just the last few years, here are the top two performing assets historically (based on average investors tax rates):

2019: Demand notes 1.93% and MINT (Pimco ST Fund) 1.58%

Late 2020: Demand notes 1.23% and High Yield Savings 0.74%

Early 2021: ST Treasuries 0.81% and Demand Notes 0.77%

Late 2022: ST Treasuries 3.12% and MINT 2.58%

Early 2023: ST Treasuries 3.38% and No Penalty CDs 3.33%

I previously stated that these securities are not how I’d recommend storing your cash. While they provided “nominal” protection – you won’t lose your principal in dollar terms, they had no ability to adjust for inflation. Instead, I’ve always recommended the Ultimate Liquidity Portfolio, explained in the book I co-wrote with Shannon Matthiesen here. Over the last several decades, that portfolio has had a better yield, with reasonable inflation and downside protection. But a once in 250 year bond market in 2022 changed the game.

In 2022 Federal Reserve demonstrated that it was willing to let real interest rates go below negative 5% and then violently react the other way. This markedly hurt the performance of the ULP, which lost almost 13% in 2022 – far more than I would have hoped for a “conservative” portfolio. As a result, I believe far more strongly that nominal protections have a role in protecting your emergency funds or other short term funding needs.

Let’s again review these investments and look at your current best options:

WHAT THESE INVESTMENTS HAVE IN COMMON

1) strong nominal protections on your money

2) reasonably consistent, low, and in some cases guaranteed interest rates/rates of return

3) The ability to get your money on short notice (possibly within minutes, although for the sake of this we are considering anything that can have its investment returned within 30 days)

7 WAYS TO STASH YOUR CASH

1. Cold hard cash For some people, it's hard to beat the appeal of cold, hard dollar bills stuffed under a mattress. It's the most liquid emergency fund you can think of. You literally lift up your mattress and grab it when you need it. Depending on how you define an emergency (nuclear meltdown), this might be the best answer for you. The issue is that you lose money to inflation over time.

2. High Yield Savings Accounts Available from online banks like Marcus, Ally Bank, and more. Their yield tends to follow a banks cost of funds minus a small discount. The federal government guarantees your account up to $250,000 ("FDIC insured"). The rates paid on high yield savings are determined by a bank's cost of funds; which is a combination of factors including federal reserve rates, deposit amounts, and more.

More recently, investing websites such as Betterment, Wealthfront, and YieldStreet have offered savings-like accounts that are outsourced to banks, that tend to be competitive. You're adding an extra layer but in some cases getting higher returns.

The interest on high yield savings accounts fluctuates with market conditions.

There are often minimum and maximum deposit requirements, as well as limits on the number of withdrawals that can be made per month.

3. No-Penalty CDs Available from some online banks, no-penalty CDs also offer nominal value protection up to $250,000. Unlike savings accounts, CDs do boast a guaranteed rate, good when rates are declining. Only no-penalty CDs or one-month CDs (currently uncompetitive) are considered as cash-like instruments; other CDs have penalty fees and/or terms longer than 30 days. If interest rates on savings accounts are declining, an equivalent rate CD will do better.

4. Money Market Accounts Available through brokerages like Fidelity, Vanguard, and others. These slightly riskier accounts invest in short term debt instruments, some of which are government backed or government linked, and some of which are viewed as very secure short term debt (for example, debt from large banks or corporations). The rates paid on money market accounts are related to the federal reserve discount rate, plus a small amount to price the risk of non-government debt if that's in their holdings. A special class of money market accounts are those that only hold tax-exempt securities called "Municipal Money Market Funds". These are usually attractive only to a small subset of individuals who are taxed at very high rates.

The rates fluctuate with the market and are not guaranteed.

5. Other liquid accounts Some companies offer products that can look and feel like a high yield savings account. Mercedes Benz offers "First Class Demand Notes" to accredited investors only, with a current interest rate of 4.75%. General Motors offers Demand Notes to all investors with a current rate of 4.75%.

The rates change with market conditions but tend to be 0.25% - 0.50% higher than competitive high yield savings accounts, although that is not the case as of this update – so there is no reason to put money there.

These are similar to bank accounts in that you have ready access to the funds. The difference is, unlike banks, you do not have a federal guarantee up to $250,000. This could matter if General Motors or Mercedes went bankrupt.

Is it secure? The companies have been around for decades, their credit ratings indicate that they have a less than 0.2% chance of going broke in a given year, even if they go broke it's not clear you would lose money, and they currently show no signs of significant financial distress.

In other words, the risk seems "priced correctly". However - will you still sleep soundly at night for that extra bit of return? GM is more likely to go bankrupt than the US government. You are getting paid (a bit) for this risk - decide whether it's worth it.

6. Cash-like funds Some exchange traded funds invest in short term debt. Examples include MINT by PIMCO, JPST by JP Morgan, and GSY by Invesco. When rates are going up these funds tend to be the first to benefit.

There is not a nominal guarantee on your money. These funds have had drawdowns (nominal losses) of up to 2.74%. Whether this feels like too much risk is up to you to decide.

Some people like these funds because they can hold instruments that are outside of the US, somewhat diversifying a US-centric risk. On the other hand, they usually don't hold US treasuries and therefore the income is almost completely taxed at ordinary income rates.

There might be some trading costs at your brokerage which can impact your profit. Also, the funds charge a fee for managing this account for you which can reduce your return.

7. Treasury bills Available through brokerages (usually without a fee), or directly from the US Government (https://www.treasurydirect.gov/RS/UN-AccountCreate.do), treasury bills are loans to the United States of America. For the sake of our analysis, we use 1 month treasuries. The rates paid are dictated by the results of federal reserve auctions.

1-month treasury bills offer nominal protection, a guaranteed rate, and are backed by the full faith and credit of the US government. Holding them directly also eliminates any risk of losing your prinicipal.

Some cash like funds hold short term US treasuries such as SHY. These funds can lose value depending on the macroeconomic environment. These funds were a casualty of last year’s inflation environment, losing up to 5.3%. If you can, you are likely better off holding short term treasuries directly.

Treasury bills (debt issued by the federal government) are not subject to state and local taxes, but are subject to federal taxes.

Money Market and cash-like funds usually lie somewhere in between. Money market funds typically hold a variety of different securities, and you will be exempt from state and local taxes on the portion that applies to you. In other words, if a fund gets 30% of its income from federal government bonds, that 30% is exempt from state and local tax. To find this out, you would search for the latest tax disclosure statement for the fund. The ratio might vary dramatically - Vanguard lists both "Federal Money Market" and "Prime Money Market" as money market funds. The former is 78% federal securities, and latter just 28%. We also talked about a special subset of funds that will hold only tax exempt securities - for example Vanguard has a "California Municipal Money Market Fund" which are not taxed at all at the federal or state level.

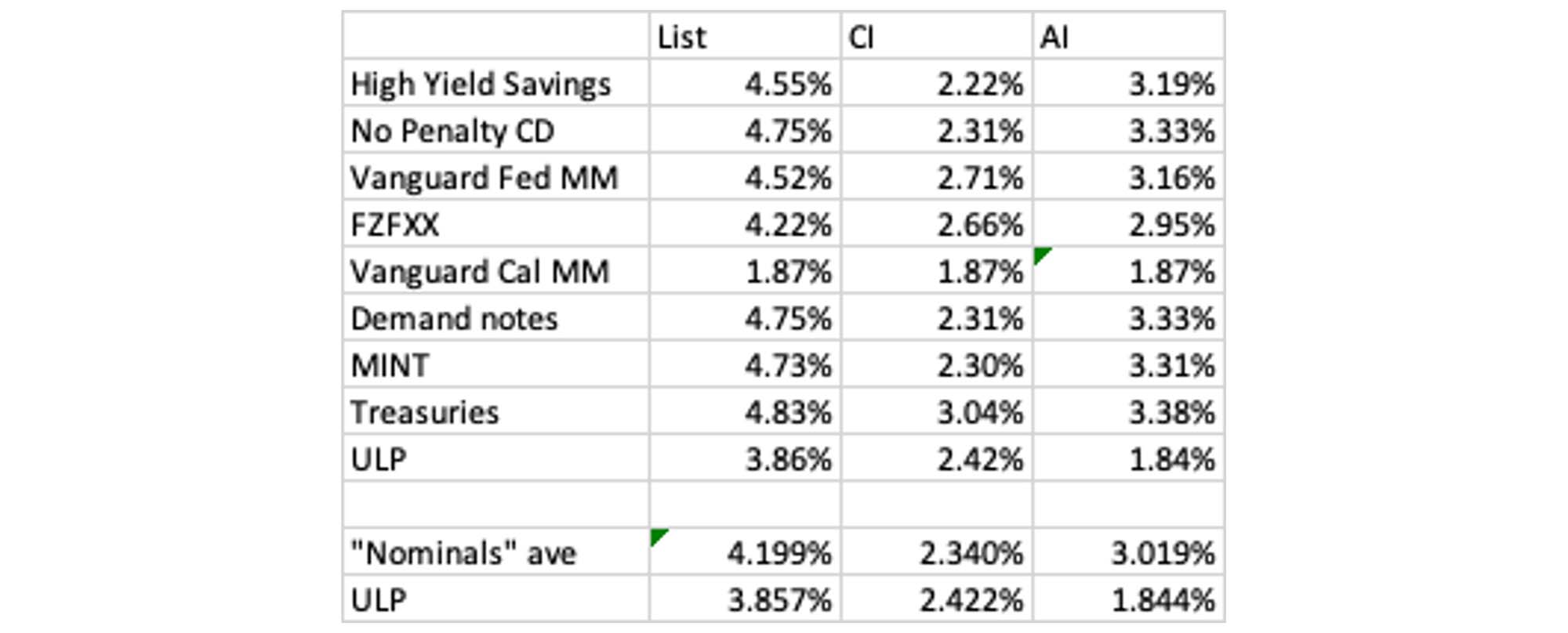

How does this play out in practice? Let's take the real world options as of today, assuming 2023 tax exposures. We'll simply list the "quoted" yield, the actual after tax yield for a high income California investor (CI), and the actual after tax yield for an "average" investor (AI) who pays 22% federal tax and 4% state tax.

Difference #2: Liquidity in crisis

All of these are extremely liquid accounts. There are a few slight differences.

Cash is available the moment you need it.

High Yield Savings accounts are typically accessible within a couple of business days.

No penalty CDs are a little slower - since there is a breakage process that needs a bit of documentation.

Money Market and cash like funds should always have liquidity to meet sales. Once sold it might take a couple of days for access. Theoretically in a full blown panic, your funds might not be available for up to a couple of weeks since you are effectively "waiting in line" for your redemption with other people.

Demand notes should act like high yield savings in most circumstances. There are some restrictions, such as minimum withdrawals and deposits, that can make the process a little less convenient. Also, similar to money market funds, in the event that everyone wants their money at the same time, it is not clear how quickly you would get paid.

Treasury Bills purchased directly, are available at expiry. In other words, if you are buying 30 day treasuries every 30 days, you would get access to the capital at the end of every 30 day period. If you bought some every day for thirty days, then the cash would be available as each treasury matures. You can also sell the treasuries (with some risk of losing some principal) if you need the cash before it expires.

SUMMARY - WHAT TO INVEST IN

In the current interest rate environment short term treasuries are the best option for guaranteeing principal plus a reasonable return, but it does not make much of a difference as rates are very close for almost all cash options. This goes for both high income and average income investors who have a 30 day horizon. Right now, only Demand notes are a silly idea – you can get a federally guaranteed return from a bank at a higher interest rate.

As I always say, it is important to continue to monitor the interest rate environment for dramatic changes.

In 2010, money market funds and treasury bills were earning less than 0.2% before taxes, while high yield savings accounts were over 1.4%. Banks still wanted deposits even though the federal government paid next to nothing for loans. If you had "set it and forget it", you would have been giving up 1.2 points of return.

For several months in 2018, treasury bills paid more after tax to most investors than either high yield savings or money market funds.

Two years ago, money market funds paid more after tax than treasury bills, but now treasury bills pay more.

My personal experience: I've invested money in high yield savings (through Marcus), short term ETFs (MINT), and money market funds (through Fidelity). Marcus frustrated me because I knew I could make more, so ultimately I've put more of my money into the other instruments.

If you want to get higher yields than those offered here, read this post.